I would say that this has been the most effective guideline for me when it comes to managing my personal finances. I used to disagree with this “It’s not how much money you make, it’s how much money you keep” and anything that says like it simply because I used to work where I got paid super low and it was insufficient for my needs and wants in life and I just thought that it wasn’t really realistic at all. But actually, it was my living above my means that was unrealistic.

In my first job after university, my pay was higher than the regular and with the incentive schemes my company had, it was actually enough for a decent living where I could also keep some of my money for saving. And then, I opted to change my job because I didn’t feel like I was growing there and so, there I was in my second not-so-high-paying job but a satisfying one. There I was with the same needs and wants not considering that how much I was making in a month wasn’t actually enough for it. That time, I wasn’t so keen on sorting nor identifying my needs vs my wants yet. Because I was somehow tailed with debts every month, I challenged myself on making it’s-not-how-much-money-you-make-but-how-much-you-keep TRUE.

I started from taking note of my expenses i.e. identifying my needs (necessities like food, water, house rent, electric bills, my data/internet (because I had some extra businesses I had to keep running that required internet connection—if it wasn’t for that my internet would have been considered as another liability and so should not be a part of my need) and etc. so anything keeping us alive–well, conveniently alive is a need) and separating my wants (wants are anything you can live without it) from it. Then, I added everything up and remember saying “Oh, so this is what I need every month. These are the things I don’t really need. ” . I put the two together and it didn’t even have room for me to have savings and investments. It was actually negative because I have had debts (well, because of the things mentioned earlier and also some circumstantial reasons (like sudden expenses like hospitalization of a loved one and what not plus my environment basically trained me that financial debts were a part of anyone’s life and was necessary and is alright, which I strongly proven not to be true now) as well. Then, my family is my everything and so if it happens that one of the members got sick and confined in the hospital again, my debts would really continue whether I like it or not.

Basically, my monthly income minus my needs and wants equaled negative which means debts Monthly income – (needs + wants) = negative or debts.

So, I was thinking, how could I ever have that saving to do the things I want to do in my life? Things like traveling, going out with friends, treating my family to a vacation and stuff like these. Determined to get out of my financial situation, in my research, I found tow important answers to my question.

1. Increase your income like find another additional source so maybe like do part time jobs or do businesses, etc..

2. Do proper budgeting.

Resourceful as I am, I did manage to find additional sources of my income (sideline selling and whatever) but then still, it wasn’t enough. Hence, I had to find out what PROPER BUDGETING really meant. Then I learned that this PROPER BUDGETING THINGY must include the following:

- Emergency Funds

- Saving and Investment

- Needs

- Wants

- Tithe (This one is basically optional depends on your principle and belief as a person but in my case, well, it’s good to give back sometimes so I believe this must be a part of me, but I don’t necessarily give it to the church or any organizations per say, I give it directly to the people who need it like street children or relatives that are not part of the budget and so on.)

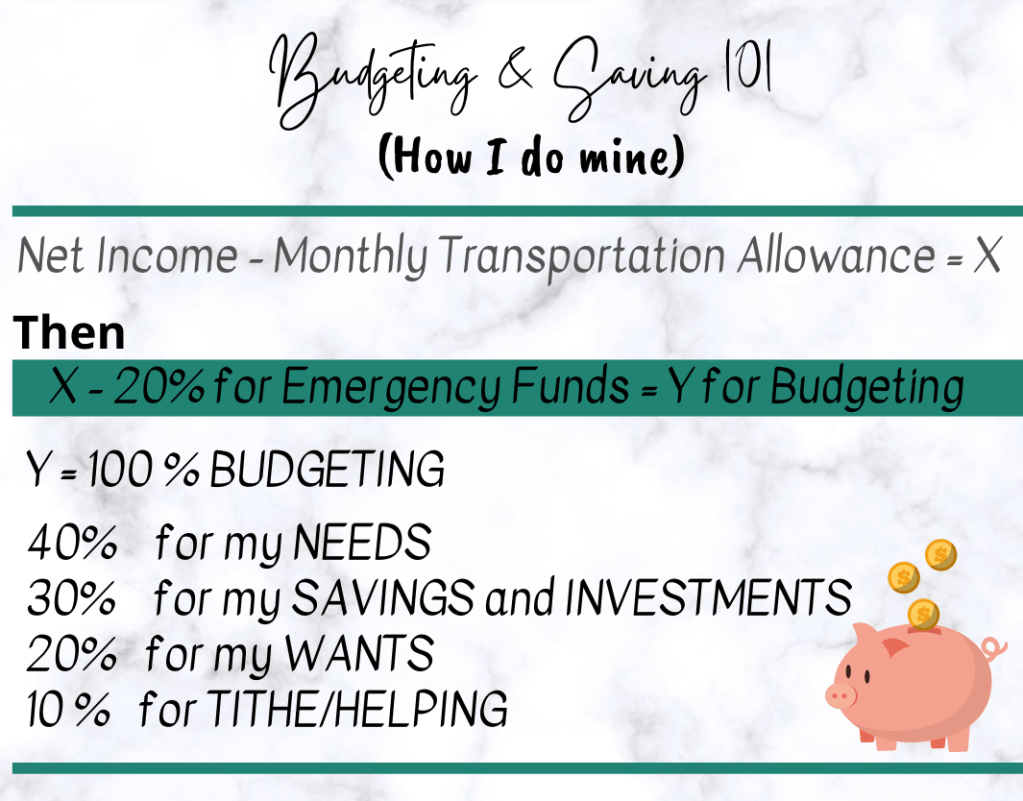

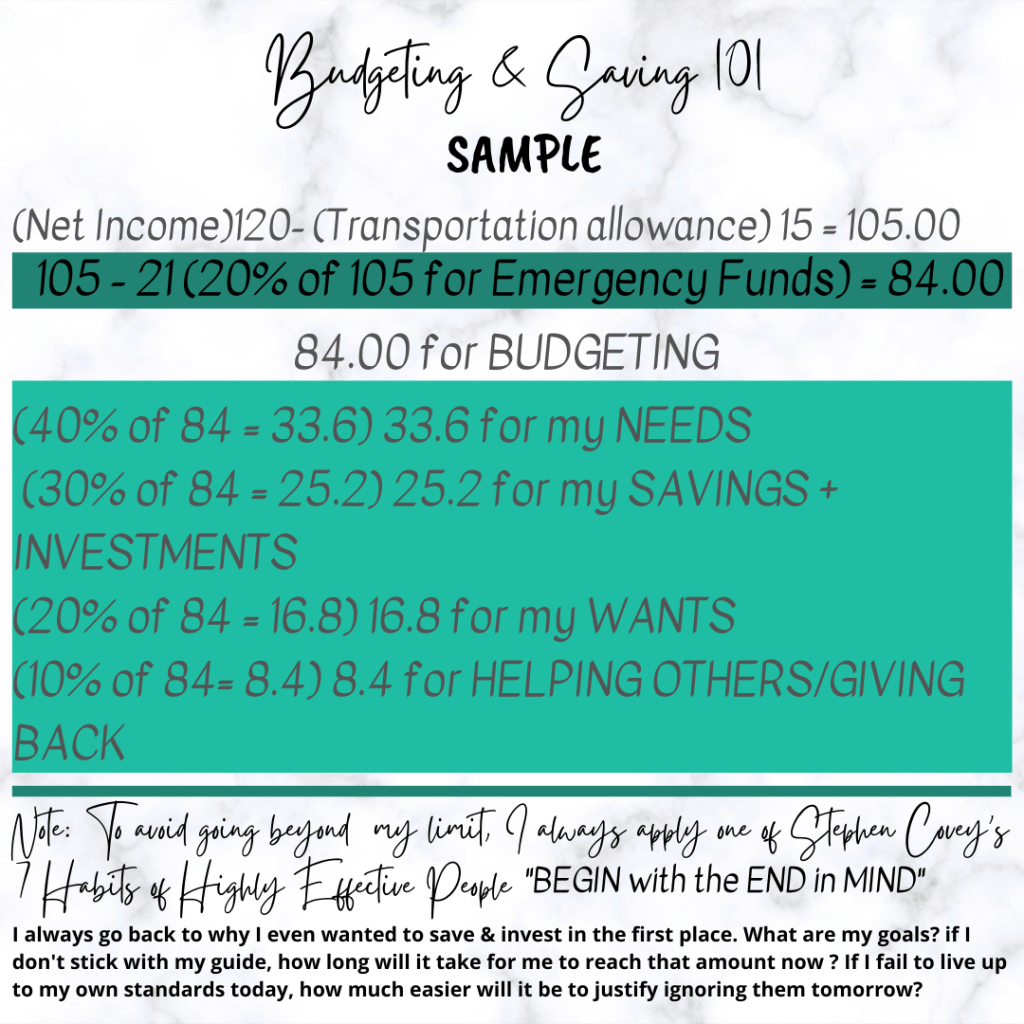

How must PROPER BUDGETING be done?

To illustrate, how I do mine, please refer to the following: (based on my current monthly income and expenses)

Anyway, after years of giving it a try and following this guideline, I finally understood and proven how effective it is just having one. I don’t feel guilty for buying and spending for what I want because at the end of the day, I know I have my savings and investments, my emergency fund (which I am continuously building up) and my budget for giving back (tithe) so when I see or encounter someone who needs help I can give if I want to.

The point being is that hopefully having a guideline as simple as this can get you started into developing a good spending habit. Good spending habit and better management of our finances can help us into reaching our dreams and doing the things we want to do in the future without having to sacrifice living-in-the-moment moments. And, the best things about having a guide is that you don’t end up overspending on something and most of the time, we tend to overspend on something that isn’t really necessary. So, at least we get to limit ourselves depending on our priorities in the present moment and our goals in the future.

READ MORE

Why TITHE? Is it really necessary?

Published on Aug 20, 2020 at 11:14 PM